Policies must favour consortiums of local players - for operators with a government stake, and for manufacturers/system integrators with market access conforming to WTO rules.

Shyam Ponappa | August 6, 2020

Two developments highlight the need for government to sponsor consortiums to build India’s digital ecosystem:

- Facebook’s announcement in April to invest $5.7 billion in Reliance Jio was momentous. In a slowing economy, Reliance Industries raised an incredible $20 billion with a cascade of foreign investments combined with a rights issue. This “consortium” makes Reliance debt-free, besides providing the capital and capacity to dominate communications in India.

- India’s digital ecosystem’s dependence on China and on increasing imports underlines the imperative for corporate India to come together in a national endeavour that must succeed.

The Jio factor

Overwhelming dominance rarely benefits the public interest, even if the pricing starts incredibly low. Developed markets frown on monopolistic dominance, despite there being giants such as Microsoft, Google, Apple, Amazon, and Facebook.1

Discounting tall talk, India’s communications sector now has these upbeat expectations, along with a slew of old negatives, particularly the debt- and tax-burdened, fragmented other operators together with recalcitrant policies. Government-imposed charges and tax battles burden our operators, rendering them unable to compete.

How have Jio’s moves affected the public interest? With both benefits and detriments. The negative fallout from sectoral debt from auctions and crippling government levies, and a price war, has been unsustainably low tariffs. A positive effect is that data traffic increased greatly because of the low tariffs. Yet, the results are damaging: For service providers because of insufficient profits, for the market because it constrains quality and growth, and, therefore, for consumers in the short and long run. Service levels are compromised by resource constraints (dropped calls, slow speeds), and because of under-served customers — both in existing and the unserved markets in India. Data traffic may have increased simply because more people watch more rubbish in video form, whereas service providers need the wherewithal to invest, to improve and extend coverage, as well as to design constructive educational, skill-building, medical services, and other enhanced interactive services for users’ genuine benefit. In that sense, traffic as a measure of user benefits can cut both ways.

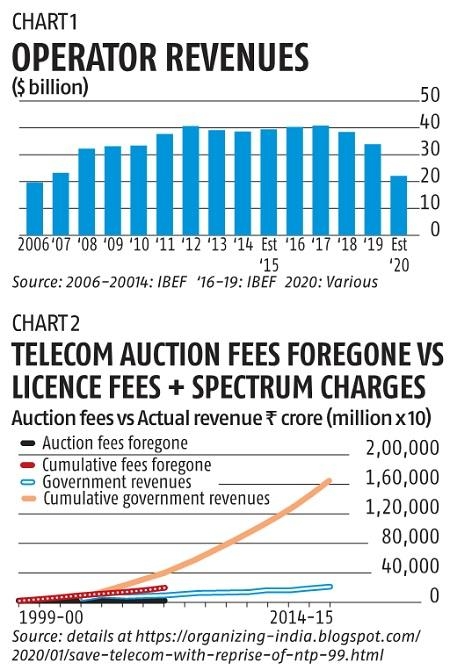

Apart from data, two other aspects merit consideration: Operator revenues, and government collections (licence fees, auction charges, and taxes). Operator revenues grew strongly from mid-2003 through FY2012, flattened for five years (FY2013-17), then declined after FY2017 (see Chart 1).

Barring additional charges, government revenues reflect this decline, leaving these lingering questions:

- Does the declining trend serve the public interest?

- What is the opportunity cost of disruption and deprivation of services?

A third issue requires action: How do we improve our digital prospects? Note that government collections from licence fees and spectrum charges rose steadily from FY2004, so that cumulative revenues far exceeded auction fees foregone (Chart 2). Corporate taxes were in addition to this.

Thereafter, government collections flattened, then declined (barring retrospective charges), as did taxes. This calls for policy intervention to enhance services, thereby increasing revenues and government collections. Straightforward adoption of global norms for wireless in 60GHz, 70-80GHz (V-band and E-band) and unused UHF (500-700MHz) restricted to operator use will help.2 So will giving up the farce of reviving BSNL/MTNL, including the hopelessly snaggled VRS, and the botched tenders (‘Most of it to Huawei?’ ‘No, Ericsson and Nokia.’ ‘Alright, 10 per cent to domestic suppliers.’ ‘No, all of it to domestic suppliers…’).

Competition for Services

A way to nurture balanced competition in services is for the government to create a consortium with a minority anchor, bringing financial, technological, and delivery capability to compete with Jio’s dominant platform.

Reliance Industries Chairman Mukesh Ambani calls for doing away with 2G; Airtel Chairman Sunil Mittal calls for supportive policies, and repudiating old battles such as contention over the adjusted gross revenue (a 15-year battle won in lower courts, lost in the Supreme Court), and reducing exorbitant charges. The government can change policies to achieve these. It can stop predatory practices, and facilitate this consortium. BSNL/MTNL can be genuinely supported to be the government anchor in the consortium with a minority stake, with golden-share national security, public- and minority-interest responsibilities through appropriate legislation. Airtel could be the lead, with others participating, including foreign players.

Equipment Consortium

Fragmented suppliers and system integrators also need a consortium for collaboration. While multinational vendors dominate, dependence on imports and China is untenable for our increasing and strategic requirements. Absent enabling policies, Indian manufacturers have to succeed offshore to sell within the country. Why do such things happen? Many reasons, starting with the holdover of colonial mindsets even of those who want to rewrite history, which treat the government — whoever is in power — as the colonial/feudal overlord, and the people as serfs with a vote, whose weaknesses can be pandered to for electoral victory. This imposes a zero-sum framework—the government versus the rest (Us versus Them).

In reality, the situation need not be zero-sum, as evidenced by past service growth and government collections through revenue sharing, compared with what might have been if auction fees were enforced: Bankruptcies and no services.

The prerequisites are (a) policies framed to provide access to local manufacturers and service providers conforming to WTO requirements; (b) their market access through continuing orders; (c) their collaboration to supply, install, and facilitate operations and maintenance of requisite equipment.

If these were made possible, domestic suppliers could meet a significant share of India’s communications needs. This requires emulating the Huawei model — easier said than done!3

The Union and state governments need to understand these components, and execute them from a national perspective, without bombastic rhetoric, politicking, fund-raising for elections, and so on. Policies must incentivise coordinated action; orders have to be winnable by including criteria for development of domestic capacity to conform to the World Trade Organization rules; and execution has to be first rate (on time, high quality). Digital communications will drive many aspects of all sectors. Our policy-makers must stop dithering and help us prepare effectively.

Shyam (no space) Ponappa at gmail dot com

1. For issues about competition laws in India, see: Amber Sinha & Arindrajit Basu, April 30, 2020:

"Analysis: Reliance Jio-Facebook deal highlights India’s need to revisit competition regulations"

"Analysis: Reliance Jio-Facebook deal highlights India’s need to revisit competition regulations"